Key takeaways

What this article covers, in order:

- Handy workflows and controls to avoid errors and speed up reconciliation

- Why AI reduces accounting errors

- Leveraging several key mechanisms to achieve 95% of of the reduction

- Designing workflows for reliable results

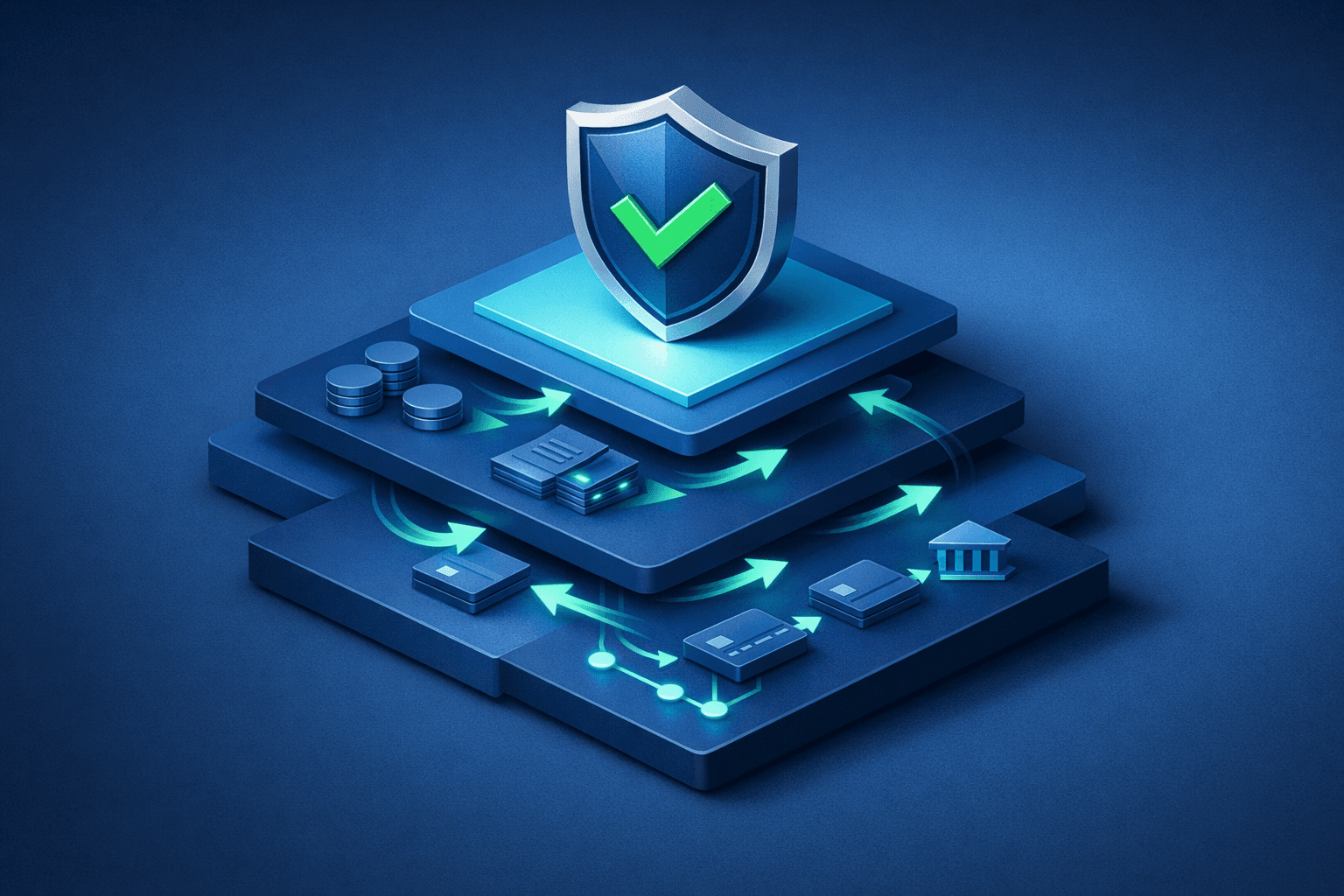

- Integration Patterns For Accounting Systems

- Data Lineage And Provenance